What is Credit, How it’s Calculate, and Why You Need It – A Comprehensive Guide

Remember getting your first credit card?! Whether it was during a college fair or at your favorite store at the mall, many of us women of color get these introductions to credit lines without having been taught what a line of credit actually means and how to use these responsibly and strategically.

Remember getting your first credit card?! Whether it was during a college fair or at your favorite store at the mall, many of us women of color get these introductions to credit lines without having been taught what a line of credit actually means and how to use these responsibly and strategically.

Credit plays a vital role in personal finances. As an adult establishing good credit matters as it will determine where you live, study, vacation, and even where you work. But have you ever wondered what would happen if you never established credit? In this comprehensive guide, we will delve into everything you need to know about credit – what it is, how it’s calculated, and why it holds immense significance in achieving financial success. By understanding the importance of credit, you can take proactive steps to build and maintain good credit, paving the way for a successful financial future.

What is Credit?

Credit refers to the creditworthiness or credit history of an individual or a company. In essence, credit is the lifeline that allows you to fulfill your financial aspirations. Good credit grants you the ability to borrow money with the commitment to repay the borrowed amount along with interest within a specified timeframe.

Now, let’s explore how credit can significantly impact your financial journey and why it’s crucial to understand its workings.

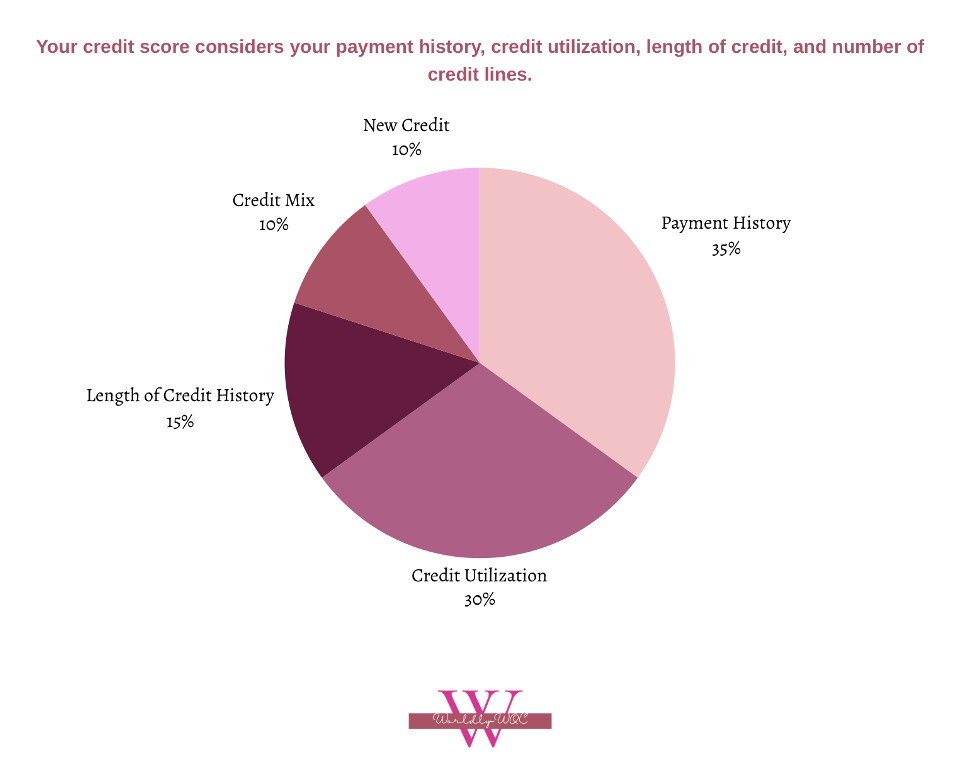

How is Credit Calculated?

Credit is a measure of your trustworthiness, reflecting the likelihood of you to pay back borrowed funds. Your credit score is a three-digit number ranging from 300 to 850 that plays a significant role in determining your creditworthiness. The higher the score, the better your creditworthiness.

Several elements come into play when calculating your credit score and understanding them is essential for improving your financial standing. Let’s explore how these factors interact and affect your creditworthiness, ultimately shaping your financial opportunities.

- Payment History: Your credit score heavily relies on your ability to make timely payments on credit accounts and bills. Even one late payment can affect your credit score. Consistently paying your bills on time can significantly boost your credit score and demonstrate responsible financial behavior to lenders.

- Credit Utilization: High credit utilization, where you use a large percentage of your credit limit, can negatively impact your credit score. As a rule of thumb, you should keep your credit utilization to 30% or less. For example, if you have a credit limit of $1,000 you should never carry a balance greater than $300. Keeping your credit card balances low and maintaining a healthy credit utilization ratio can improve your creditworthiness.

- Length of Credit History: The length of your credit history matters; a longer credit history provides more data for creditors to assess your creditworthiness. There’s not much you can do here besides be patient and maintain good credit practices over time to build a strong credit history.

- Credit Mix: A diverse credit mix, which includes a variety of credit types such as installment loans (where you borrow a one time lump sum) and revolving credit (where you borrow as you please up to a set credit limit), can positively influence your credit score. A well-balanced credit portfolio shows that you can handle different types of credit responsibly.

- New Credit: Opening several new credit accounts can raise concerns for lenders, potentially lowering your credit score. When asked for your credit history, understand whether it will be a hard inquiry, meaning it will be reported in your credit history. Minimize hard credit checks and only apply for credit when necessary to maintain a healthy credit profile.

- These five factors combined determine your credit score. Understanding the intricacies of credit score calculation empowers you to take charge of your financial well-being. By being aware of these factors, you can make informed decisions and take proactive steps to improve your creditworthiness, opening doors to better financial opportunities and achieving your long-term goals.

Why Do I Need Credit?

Credit is an indispensable tool that grants access to financial resources, making it possible to achieve dreams like owning a home or starting a business. Good credit brings lower interest rates, leading to substantial long-term savings. Additionally, it influences various aspects of life, such as securing rental apartments or better job opportunities. With a strong credit profile, one gains access to a wide range of financial products and services, ensuring better financial management. Moreover, credit acts as a safety net during emergencies, providing the funds needed to navigate unforeseen circumstances. Understanding the importance of credit empowers individuals to use it responsibly.

Ways to Improve Your Credit:

- Check Your Credit Reports – Obtain free credit reports from all three major bureaus (Equifax, Experian, and TransUnion). Review them for inaccuracies, such as incorrect accounts or late payments, and dispute any errors you find.

- Pay Bills on Time – Consistently make on-time payments for all your bills, including credit cards, loans, and utilities. Late payments can significantly impact your credit score.

- Reduce Credit Card Balances – Work on lowering your credit card balances to reduce credit utilization. Aim to keep your credit card utilization below 30% of your available credit.

- Limit New Credit Applications – Opening multiple new credit accounts in a short period can lower your score. Only apply for credit when necessary, and avoid excessive inquiries.

- Build Positive Credit History – If you have limited credit history you can consider becoming an authorized user on someone else’s credit card. This will allow you to benefit from their credit history, but this person would be responsible for any purchase you make on their credit line so it is important to use this cautiously. You can also apply for a secured credit card, which requires a cash deposit usually in the amount of the credit limit you’re seeking. Once you’ve established a good credit history your credit lender will refund you your deposit and you’ll have a traditional credit card.

- Prioritize Debt Repayment – Create a plan to pay off high-interest debts first. Focus on reducing outstanding balances on credit cards and loans with higher interest rates.

Credit is a crucial aspect of personal finance that profoundly affects your access to financial resources and ability to achieve your goals. By understanding what credit is, how it’s calculated, and why it’s important, you can take steps to build and maintain good credit, paving the way for financial success. For more information on how to improve your credit and take control of your financial future, be sure to check out our other blog posts here at WorldlyWOC!