Crushing Student Debt: Your Roadmap to Thrive Beyond Loans

In a recent landmark decision, the Supreme Court overturned President Biden’s student loan forgiveness program, leaving countless borrowers uncertain about their financial futures. The program, which aimed to provide relief to millions of struggling borrowers, has now been shut down. As a result, many students, graduates, and particularly women of color across the nation are nervously awaiting the end of the payment pause on their student loans. Interests on federal student loans are set to resume in September 2023 and the first payment will be due the following month in October 2023.

In a recent landmark decision, the Supreme Court overturned President Biden’s student loan forgiveness program, leaving countless borrowers uncertain about their financial futures. The program, which aimed to provide relief to millions of struggling borrowers, has now been shut down. As a result, many students, graduates, and particularly women of color across the nation are nervously awaiting the end of the payment pause on their student loans. Interests on federal student loans are set to resume in September 2023 and the first payment will be due the following month in October 2023.

With this reality in mind, it is crucial for all borrowers, but especially those from marginalized communities, to stay informed and plan to take action. Understanding your student loans is the first step towards financial empowerment.

Understanding Your Student Loans

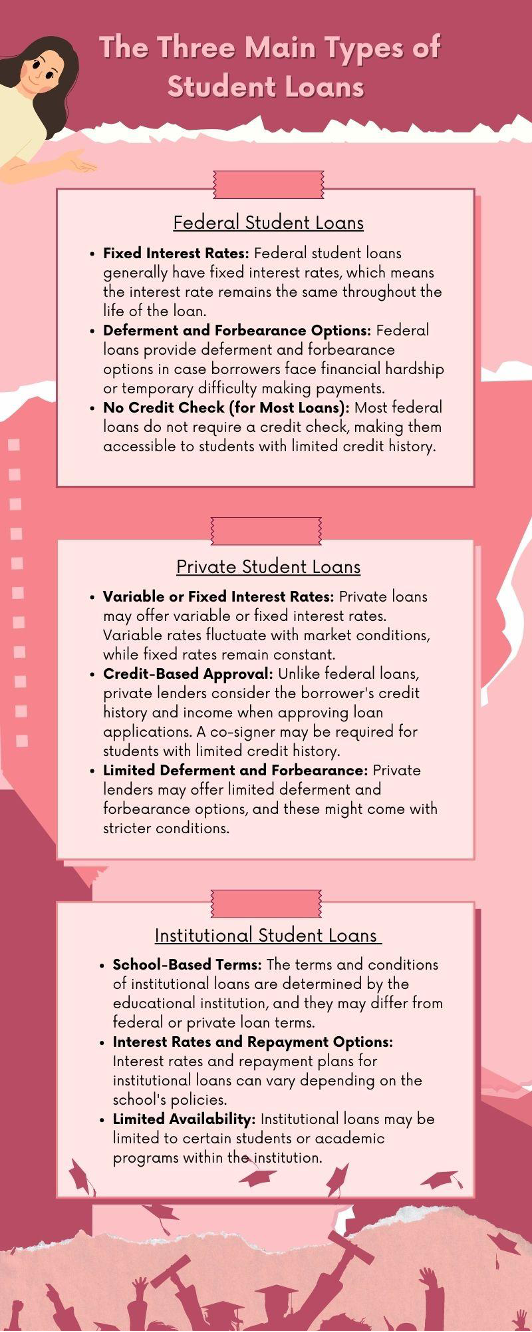

Student loans have become a crucial aspect of financing higher education for millions of students. These loans provide financial assistance to cover tuition fees, living expenses, and other educational costs. There are three main types of student loans: federal, private, and institutional. Each type has its unique features and considerations, and understanding the differences can help students make informed decisions about their financial future.

Federal Student Loans

Federal student loans are offered by the U.S. Department of Education and are the most common type of student loans. These loans come with various repayment options, forgiveness programs, and protections such as:

- Loan Forgiveness Programs: Certain federal loan programs, such as Public Service Loan Forgiveness (PSLF), offer loan forgiveness after a specified period of qualifying payments; and

- Income-Driven Repayment Plans: Borrowers have the option to choose income-driven repayment plants where monthly payments are adjusted based on the borrower’s income and family size.

- Subsidized loans: The government covers the interest on subsidized loans while you’re in school and during deferment, making them more affordable. Unsubsidized loans start accruing interest immediately, regardless of financial need, and this interest is added to the loan balance, making them more costly in the long run.

One of the great aspects of federal student loans is the deferment and forbearance options.

Deferment

Deferment refers to a temporary postponement of payment on a loan during which interest generally does not accrue on subsidized loans. There are many different types of deferment options including Economic Hardship, In-School, and Graduate Fellowship deferments.

Forbearance

Similarly, forbearance is a temporary break from student loan payments, but interests still accrues while you’re in forbearance. This makes it a less-ideal choice when you’re facing hardship and stress over making payments, but it’s a good option to avoid defaulting on your loan if you’re unable to pay. Forbearance options are available if you are faced with financial difficulties, medical expenses, change in employment, or other reasons acceptable to your loan servicer.

Most deferments and forbearance options are not automatic—you need to submit a request to your student loan provider as well as supporting documentation for your request.

Private Student Loans

Private student loans are offered by banks, credit unions, and other private lenders. These private loans often have higher interest rates and fewer repayment options. Private student loans are not subsidized or regulated by the government, and the terms and conditions can vary significantly between lenders.

It is important to note, that unlike federal student loans, many private lenders do not provide any deferment or forbearance options.

Institutional Student Loans

Institutional student loans are provided by colleges or universities directly. These loans are governed by the college or university that is offering them. The terms of these loans vary and it is important to contact your school to make sure you understand these terms before agreeing to assume a loan.

Choosing the right type of student loan is an important decision that can significantly impact a student’s financial future. Before taking out any student loan, students should research and compare their options, considering factors such as interest rates, repayment terms, and available benefits. You can start your research by visiting studentaid.gov. Consulting with a financial aid advisor or loan counselor can also provide valuable guidance in making the best decision based on individual circumstances.

Should You Refinance Your Student Loans?

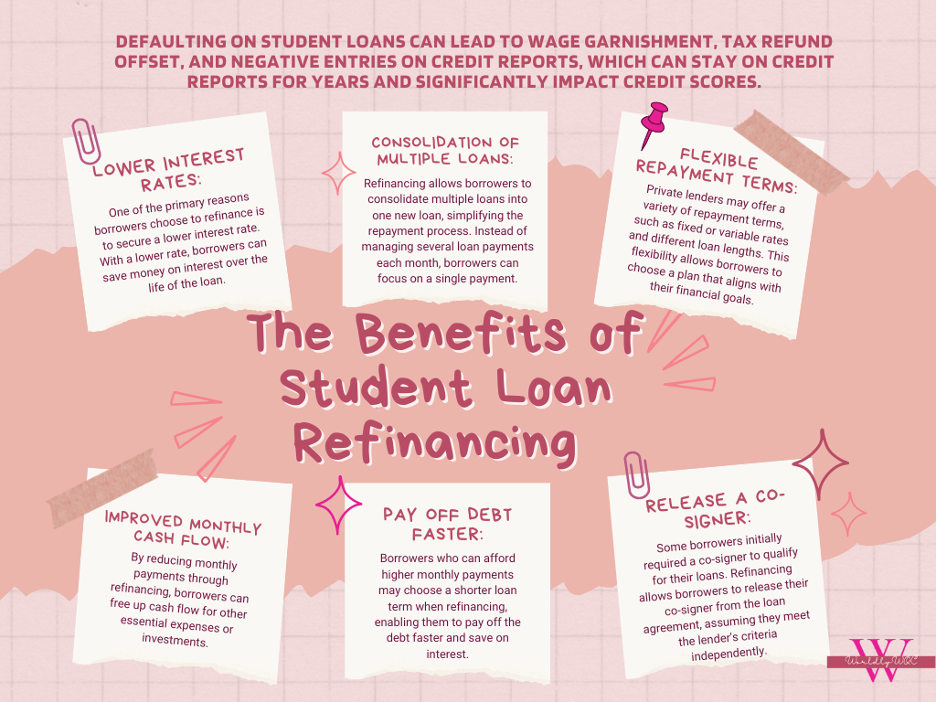

Student loan refinancing is a process that allows borrowers to replace their current loans with a new loan from a private lender. The new loan usually comes with different terms, such as a lower interest rate or a different repayment schedule. Refinancing can be beneficial for borrowers who want to lower their monthly payments, save on interest, or consolidate multiple loans into one.

Managing student loan debt can be challenging, especially for recent graduates and young professionals. Many borrowers find themselves burdened with multiple loans, each with different interest rates and repayment terms. This situation can make it difficult to keep track of payments and may result in higher overall interest costs. Refinancing offers a solution to simplify and potentially improve the loan terms, providing borrowers with more manageable and affordable repayment options.

Before considering refinancing, borrowers should assess their financial situation and creditworthiness. Refinancing often requires a good credit score and stable income. Having a good credit score will result in more favorable refinancing options. However, it’s essential to remember that refinancing federal loans with a private lender may cause borrowers to lose certain federal loan benefits, such as income-driven repayment plans, loan forgiveness programs, and deferment and forbearance options. Thus, borrowers should carefully weigh the advantages and disadvantages before proceeding with the refinancing process.

How to Refinance Your Student Loans

The refinancing process begins with researching and comparing different lenders and their loan offers. Borrowers should review interest rates, repayment terms, and any associated fees before making a decision. Online comparison tools and loan calculators can be valuable resources in this phase, helping borrowers assess various offers side by side.

Once a suitable lender is found, borrowers can start the application process. This involves providing personal and financial information to the lender for evaluation. The lender will consider factors such as credit history, income, and employment status to determine eligibility and the terms of the new loan.

It is essential to note that applying for multiple refinancing options within a short period can lead to multiple hard inquiries on your credit report. This may temporarily lower your credit score, so borrowers should time their applications strategically.

If approved, the new loan will replace the existing ones, and borrowers can begin making payments according to the new terms. It’s crucial to adhere to the new payment schedule and avoid missing any due dates to maintain a positive credit history and continue reaping the benefits of refinancing.

With the right approach, refinancing can offer significant benefits, helping borrowers achieve their financial goals and gain control over their student loan debt.

Are Student Loans “Good Debt”?

The simple answer is not really. Many people describe student loan debt as “good debt,” but this can be misleading. While student loans help you get a college education, which increases your lifetime earning potential, these are still financial burdens you must deal with.

Further, student loans can have a significant impact on borrowers’ credit scores, both positively and negatively.

Student loans are often the first substantial credit obligation that many young adults take on. As such, when managed responsibly, student loans can provide a valuable opportunity to establish a credit history and improve credit scores. However, mishandling student loans can have adverse effects. Late payments, defaulting on loans, or allowing loans to go into collections can severely damage credit scores. Defaulting on student loans can lead to wage garnishment, tax refund offset, and negative entries on credit reports, which can stay on credit reports for years and significantly impact credit scores.

It is essential for borrowers to strike a balance between using student loans to invest in education and managing debt responsibly. Students should avoid borrowing more than necessary and consider their future earning potential before taking on student loan debt. This means being mindful of the loan amount and choosing the most suitable repayment plan based on your financial situation. For example, income-driven repayment plans can be beneficial for borrowers who expect to have lower incomes initially but anticipate higher earnings in the future.

Making informed financial decisions and being proactive in loan management can ensure that student loans positively contribute to your overall financial wellness.

Tips to Manage your Student Loans Effectively:

- Know Your Numbers: I know that it is easy for many of us women of color to avoid looking at our debt, because it can be intimidating. But the first step to financial freedom is financial awareness. Look at your numbers, allow yourself to sit in the discomfort that it may bring you, and create a plan to tackle your debt!

- Know Your Loan Provider: Federal student loans typically have different loan servicers that handle repayment and customer service. Understanding which loan servicer manages your loans can help you navigate repayment options effectively.

- Create a Budget: Establish a budget that includes monthly student loan payments.

- Set Up Auto-Pay: Consider setting up automatic payments for your student loans to ensure on-time payments and avoid late fees. Many loan providers will also give you a small discount for setting auto-pay.

- Monitor Your Credit: Regularly review your credit reports to check for accuracy and identify any potential issues that may impact your credit score.

- Stay Informed About Repayment Options: Understand the various repayment options available for your student loans and choose the one that aligns best with your financial situation.

- Avoid Default: If you encounter financial difficulties, contact your loan servicer to explore options like deferment, forbearance, or income-driven repayment plans to avoid default.

- Pay More Than the Minimum: If possible, consider paying more than the minimum required monthly payment to reduce the overall interest paid and pay off the loan faster.

- Seek Financial Assistance: If you’re facing financial hardship, seek assistance from a financial advisor or counselor who can provide guidance on managing student loans and improving credit. Click here to work with me!

Consequences of Failing to Pay Your Student Loans

Defaulting on student loans can have severe consequences for borrowers. Student loan default occurs when borrowers fail to make payments for a specified period, usually around nine months for federal student loans. When borrowers default, their loans are sent to collections, and they become subject to wage garnishment, where a portion of their wages is withheld to repay the debt.

Additionally, defaulting on student loans can lead to a tax refund offset, where the government seizes the borrower’s tax refund to repay the debt. This can significantly impact borrowers’ financial stability and prevent them from using tax refunds for other essential expenses.

Defaulting on student loans also results in negative entries on borrowers’ credit reports. These negative entries can stay on credit reports for up to seven years, making it challenging to rent an apartment, and secure new credit, such as mortgages, credit cards, or car loans. To avoid default, borrowers should explore alternatives such as income-driven repayment plans, deferment, and forbearance.

As you navigate the world of student loans, it’s essential to be well-informed and proactive. Understanding your student loans is the first step towards financial empowerment. By understanding your loans, considering refinancing options, and managing your credit responsibly, you can thrive beyond student loans and build a strong financial future.